How to Source Pre-Seed Deals Before the Pitch Deck Exists

Most venture capital sourcing advice starts too late. It assumes founders already have a company, a product, and something to show. It focuses on inbound deal flow, warm introductions, and database searches, all of which share the same flaw: by the time a founder appears through any of those channels, the window for a truly early entry has already closed.

This guide is about what happens before any of that. It is about finding founders at the moment of formation, not the moment of fundraising.

What "Early" Actually Means in VC Sourcing

Pre-seed investing is often described as the earliest stage of institutional venture capital. But within pre-seed, there is enormous variation in how early different investors actually get in.

At one end, a fund catches a company three months before the seed round closes. The founder has a deck, a demo, and a growing list of interested investors. This is "pre-seed" in name, but the competitive dynamic looks exactly like a seed process.

At the other end, a fund reaches a founder two weeks after they incorporated, before they have hired anyone, before they have a product, and before they have told anyone outside their immediate network what they are building. This is pre-seed in the truest sense, and the conversations are entirely different.

The practical difference between these two scenarios is not just valuation. It is relationship. A founder who is approached when they are still figuring things out has time to think about which investors they actually want on their cap table. A founder in the middle of a process is optimising for speed and terms.

The funds that consistently find founders at the formation stage do not stumble onto them through luck. They have built systematic sourcing infrastructure that surfaces signals before any public announcement.

Why Traditional Sourcing Methods Are Structurally Late

Understanding why traditional sourcing is late helps clarify what needs to replace it.

Inbound deal flow is the most extreme case. A founder who sends a cold email or fills out an application form has already decided to fundraise, has probably already started conversations elsewhere, and is at minimum several months into building. The investor receiving that email is not early. They are one of many.

Warm introductions are better, but not by as much as most funds assume. A mutual contact introduces a founder when the founder asks them to. That request typically comes when fundraising has begun or is imminent. The introduction may feel exclusive, but the same founder is probably asking for five similar introductions simultaneously.

Accelerator and program pipelines compress the timeline somewhat, but the same logic applies. By the time a founder has applied to, been accepted by, and progressed through an accelerator, they are visible to every investor in that program's network. Early by some definitions. Not early in the sense that matters most.

Database and platform searches, including Crunchbase and Dealroom, reflect reality as it was when the data was collected. Even the most up-to-date databases lag the real world by weeks or months. A company that appears in a search has enough public information to be indexed. That is already too late.

The common thread is that all of these methods are reactive. They require a founder to do something visible before the investor can act. The earliest funds have inverted this: they find founders before any visible action has been taken.

The 6 Signal Types That Surface Founders at Formation

Founders leave traces before they announce anything. Not deliberately: these traces are byproducts of the practical steps required to start a company. A founder detection approach monitors these signals systematically to identify company formation as it happens.

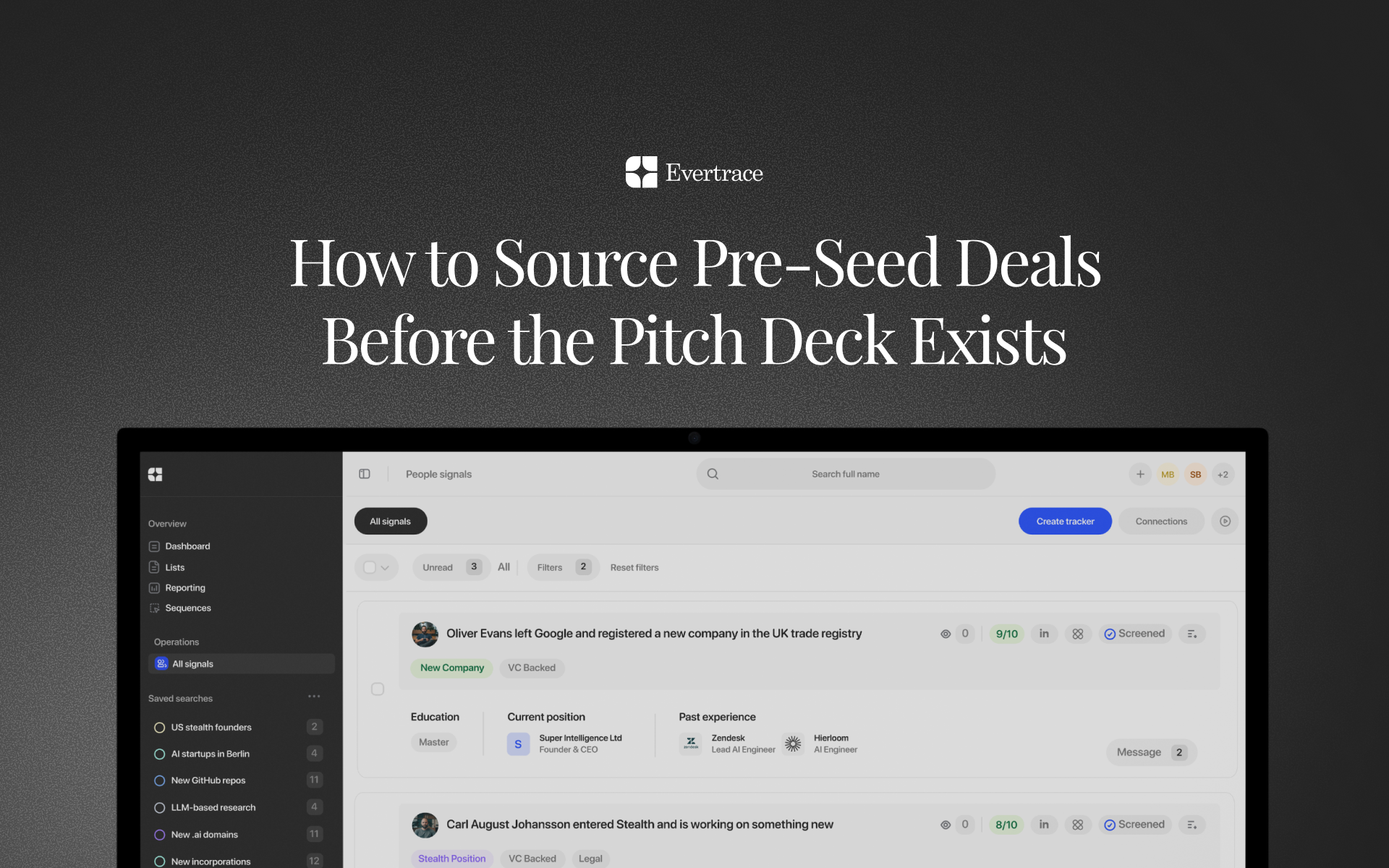

1. Trade registry filings

Incorporating a company is often the first concrete step a founder takes. In Europe, new incorporations are publicly recorded in government commercial registries: Companies House in the UK, the Handelsregister in Germany, the KVK in the Netherlands, and equivalents across most European countries.

A new filing from an individual with a relevant background, in a relevant geography, is a meaningful signal. The challenge is volume: hundreds of thousands of new companies are registered in Europe each year, the overwhelming majority of which have nothing to do with venture-backable technology startups. Effective sourcing requires filtering these filings in real time to isolate the ones that matter, linking incorporation records to individual founders, cross-referencing their backgrounds, and filtering out holding structures and non-operational entities.

2. GitHub activity patterns

Engineers who are transitioning from employment into building a startup leave detectable patterns in their code activity. New repositories appearing alongside shifts in commit frequency and timing, changes in the type of work being built, and other behavioral signals can indicate that someone is moving from professional work to independent building.

This signal is particularly valuable for technical founders building developer tools, infrastructure, or other software products. A strong engineer who begins pushing meaningful code to new repositories outside working hours, with increasing intensity over several weeks, is exhibiting a pattern that looks very different from a hobbyist side project.

3. Patent filings

When an individual or small team files a new patent, especially in a technical domain and outside the context of an established employer, it can indicate the early formation of a deep tech company. Patent filings are public records that appear weeks or months before any company announcement.

This signal is particularly relevant for deep tech, biotech, hardware, and climate verticals, where intellectual property is often developed before commercial activity begins. Tracking new patent filings from individuals whose backgrounds suggest commercial intent surfaces spinouts and research-driven ventures at a stage when most investors have no idea they exist.

4. Domain registrations

Registering a domain is a low-friction, early step that many founders take before they have a product, a team, or even a clear company name. New domain registrations can be linked to individuals through registration records, and cross-referenced with other signal types to build a fuller picture.

A domain registration alone is a weak signal. Combined with a trade registry filing and GitHub activity from the same individual within a short time window, it becomes a strong one. The value of domain signals is in how they combine with others, not in isolation.

5. Academic research and grant awards

Researchers whose published work has clear commercial potential represent a specific and valuable signal type. Academic papers in areas like machine learning, materials science, synthetic biology, or energy storage often precede commercial applications by months or years. Tracking authors who are producing commercially relevant research, and then monitoring whether they transition from academia toward company formation, gives investors a long lead time on some of the most technically significant opportunities.

Grant awards follow a similar logic. A research grant in a commercially relevant area, awarded to an individual without a current company affiliation, can signal early-stage venture formation before any incorporation has occurred.

6. Co-founder searches and social signals

Founders looking for co-founders, posting in startup communities, or signaling venture intent through social behavior leave traces that are detectable at scale. A developer posting in a co-founder matching community, or an engineer asking questions in startup forums, are behavioral signals that indicate early-stage company formation.

These signals require careful interpretation. Not every co-founder post leads to a funded startup. But combined with other signal types, they add a layer of social and behavioral context that strengthens the overall picture.

Turning Signals into Outreach That Converts

Finding founders early only creates an advantage if the outreach that follows is appropriate for the stage. An investor who reaches out to a founder in the first days of company formation and leads with "I'd love to see your deck" has missed the point entirely.

Early outreach should reflect the stage. The founder does not have a deck. They may not have a co-founder. They are still figuring out what they are building and whether it is worth building. The investor's job at this stage is not to evaluate. It is to be useful.

A few principles that work consistently:

Lead with the signal, briefly. Let the founder know how you found them without being invasive about it. "I saw you recently incorporated and noticed your background in X" is honest, specific, and shows you did your homework. It also distinguishes the outreach from generic investor spam.

Ask a genuine question. Rather than asking "are you raising?", ask something that shows you have thought about the space. "I've been following the intersection of X and Y, curious what you're working on" invites a conversation rather than demanding a pitch.

Offer something useful. At pre-formation stage, the most valuable things an investor can offer are introductions, domain expertise, and perspective. Leading with what you can give rather than what you want to assess changes the dynamic of the conversation.

Be patient with the timeline. A founder you reach two weeks after incorporation may not raise for another year. The goal of early outreach is relationship, not transaction. The transaction comes much later, and only if you have been genuinely useful in the meantime.

What a Signal-Based Sourcing Week Looks Like

For funds that have built signal-based sourcing into their process, the day-to-day looks different from a fund relying on inbound and introductions.

A typical week might involve reviewing a curated feed of new signals filtered by geography, sector, and founder profile: new incorporations in Nordic countries in deep tech, GitHub activity from engineers with backgrounds in enterprise software, patent filings from former research scientists in materials science. Most signals are noise, even after filtering. A team that reviews fifty signals a week and converts two or three into genuine conversations is operating at a high signal-to-noise ratio.

Those two or three conversations are not pitch meetings. They are introductory calls with people who are in the earliest stages of figuring out what they want to build. Some will never raise. Some will pivot multiple times before landing on something fundable. A small number will become the most important investments the fund makes.

The discipline required is patience. Signal-based sourcing creates a pipeline of pre-formation relationships, not a pipeline of investment-ready companies. The value compounds over months and years, not weeks.

Building the Infrastructure

Effective signal-based sourcing requires three things: data coverage, scoring, and workflow integration.

Data coverage means monitoring enough signal sources, across enough geographies, that relevant founders do not fall through the gaps. A fund focused on European pre-seed that monitors only trade registries will miss founders who are building in stealth without yet incorporating. A fund that monitors only GitHub will miss non-technical co-founders. Coverage breadth matters.

Scoring means having a way to prioritise signals by relevance. Not every new incorporation is worth attention. A system that ranks signals based on how closely a founder's profile matches the characteristics of previously successful venture-backed founders reduces the manual triage required and helps analysts focus on the highest-probability opportunities.

Workflow integration means signals flowing directly into the tools the investment team already uses. If a new signal requires manual copy-paste into a CRM, it creates friction that degrades the process over time. Integration with Affinity, Attio, or similar tools ensures that every relevant signal becomes a trackable relationship, not a lost note in someone's inbox.

The Compounding Advantage

The funds that have built signal-based sourcing into their process consistently report the same observation: the advantage compounds.

In the first year, signal-based sourcing produces a small number of early relationships that would not have come through traditional channels. Some of those relationships lead to investments. Most do not yet.

Over time, founders who were reached early and treated well refer other founders. Investors who are known to show up before anyone else build a reputation that compounds into more inbound interest from exactly the founders who value that kind of investor. The sourcing infrastructure produces not just early access to specific companies, but a durable reputation as the fund that finds people first.

That reputation is not built through marketing. It is built through the consistency of showing up early, being useful, and not wasting founders' time.

How Evertrace Supports Signal-Based Sourcing

Evertrace is built specifically for investors who want to source at the formation stage. It monitors real-time signals across trade registries across Europe, GitHub, patent filings, academic research, domain registrations, app stores, Product Hunt, and social platforms, connecting signals across sources to surface founders before they have announced anything publicly.

Signals are scored based on similarity to the profiles of previously successful venture-backed founders and can be filtered by geography, sector, signal type, and thesis criteria. New signals flow directly into Affinity or Attio, and the platform connects to AI agents via MCP for teams that want to automate parts of the outreach and enrichment workflow.

175+ VC firms across Europe use Evertrace to find founders before their competitors do.

Book a demo to see how Evertrace works in practice

Frequently Asked Questions

What is pre-seed sourcing?

Pre-seed sourcing is the process of identifying and building relationships with founders before they have raised institutional funding, ideally before they have even begun a fundraising process. The earliest pre-seed sourcing happens at or before the point of company formation.

How do VCs find startups before they raise?

The most effective early-stage investors combine signal monitoring across multiple data sources, including trade registries, GitHub, patent filings, and domain registrations, with systematic outreach to founders at the formation stage, before any public announcement.

What signals indicate a founder is forming a company?

The strongest signals combine multiple data points: a new company incorporation, a new domain registration, and increased GitHub activity from the same individual within a short time window. Individual signals are weaker; combinations are significantly more predictive.

How early is too early to reach out to a founder?

There is no such thing as too early, provided the outreach is appropriate for the stage. Reaching out to a founder two weeks after incorporation with an invitation to pitch is inappropriate. Reaching out with a genuine question about what they are working on is not. The earliest outreach should be conversational, not transactional.

What is the difference between pre-seed sourcing and deal flow?

Deal flow typically refers to companies that are actively seeking investment. Pre-seed sourcing at the formation stage precedes deal flow entirely. The founders being contacted may not yet have decided to raise, may not have a product, and may still be in the process of forming a company. The relationship begins before there is a deal to flow.

How do the best early-stage VCs build sourcing advantages?

The most consistently early funds combine systematic signal monitoring with a reputation for being useful before asking for anything. The infrastructure surfaces founders early; the approach to those conversations determines whether early access converts into preferred investor status.

The founder detection engine for VCs

AI-powered founder detection with unmatched coverage.

Book a demo

Book a demo